Capital markets union: be careful what you wish for…

November 2014 • Unlocking capital markets • by William Wright

Capital markets union is a great idea in need of some concrete policies. It could have a transformative effect on the European capital markets and on economic growth, but there is a danger that it could be diverted, delayed or even derailed. Here’s how:

You should be careful what you wish for, because you might just get something that looks quite like it. Ever since Jean-Claude Juncker first mentioned ‘capital markets union’ earlier this year, different constituencies across the financial markets have been busy trying to articulate their own version of what they would like to it to mean as they jockey for political position.

The danger when you have a blank canvas and so many different people wanting to paint so many different things on it at the same time is that the end result will look like something by Jackson Pollock but without the artistic merit.

As senior European policymakers meet in Brussels today to start to hammer out what capital markets might look like, here are 10 ways in which capital markets union could be diverted, delayed or even derailed…

(This article has three parts: first, a 10 point summary of potential pitfalls. Second, a more detailed look at each of those 10 points. And third, a summary of the dozens of recommendations and policy suggestions that have been made so far…)

PART 1 – SUMMARY

1 – A second order problem

Capital markets union cannot dig Europe out of its hole single-handedly. Unless governments engage in more fundamental structural reforms, there is a danger that the European economy will continue to slide sideways – and capital markets union will become a second order problem and be kicked into the long grass.

2 – If it ain’t broke…

There is a danger of assuming that everything about capital markets in Europe needs fixing. But many parts of the capital markets in Europe work well: big investment grade issuers do not have a problem tapping the capital markets, and this year the value of equity issuance in Europe is around 15% higher than in the US and the value of European IPOs is a third higher.

3 – Laundry list

Capital markets union could rapidly descend into an unwieldy laundry list that would get lost in its own complexity (we identified 99 different policy recommendations from a quick look at five separate reports). Instead it would be better to select a handful of tactical reforms that are a) achievable and b) have a concrete, measurable and significant impact.

4 – Too much regulation

There are plenty of people in Brussels for whom no problem is so complicated that it cannot be solved without more regulation or another directive. Add to that the reflexive urge of many politicians to regulate and you have a recipe for a potential barrage of new regulation that would kill capital markets union before it even got started.

5 – Too ambitious

Capital markets union is not an opportunity to solve problems that have eluded policymakers since the Treaty of Rome in 1957. Try to do much (or trying to do it too soon) – for example, by trying to harmonise entire swathes areas of tax and company law – would be a recipe for failure.

6 – Not ambitious enough

Equally, the Commission might take one look at the sheer scale and complexity of the problem and decide that it would far safer just to finish off what has already been started in terms of a single capital market, and perhaps tinker at the edges with some achievable but unspectacular reforms.

7 – The wrong diagnosis

If you misdiagnose the problem then it is unlikely that the treatment will work. Too much focus on primary markets (rather than the secondary markets needed to support them), or automatically assuming that the decline in bank lending is a catastrophe that is starving healthy SMEs of credit, is unlikely to lead to effective policy responses. Too much focus on ‘union’, and not enough on ‘capital’ and ‘markets’, could also generate a lot of unproductive activity.

8 – Diving in headfirst

Filling whatever funding gap may exist in Europe is not as easy as it looks. Direct lending by institutional investors is harder than it looks, crowdfunding is great but even if it doubles every year it will scarcely dent the market. Don’t forget that dedicated stockmarkets for SMEs and growth stocks have been tried before. Easdaq, anyone?

9 – Playing politics

Politics can always make things worse. Some ideas which have already captured the political imagination – such as the securitisation of SME loans or initiatives to build growth stockmarkets – could be rushed through the system in order to show that ‘something is being done’. Reform could also become politicised, with pensions assets being ‘allocated’ for infrastructure investment.

10 – Circular firing squad

The financial markets industry could shoot itself in the foot by using capital markets union as an excuse to sidestep painful reforms. Unless all sectors of the industry make concrete efforts to rebuild trust and overcome internal squabbling, it is unlikely that policymakers will feel the need to champion them or give them the hearing they deserve.

PART 2 – IN DEPTH: HOW TO DERAIL CAPITAL MARKETS UNION

Related content:

Why you should care about capital markets union – October 2014

Driving growth: making the case for better capital markets – September 2014

Making the positive case for capital markets – June 2014

1- Second order problem

Capital markets can play a part in encouraging growth but they cannot dig Europe out of its hole single-handedly and they certainly can’t do so by tomorrow. Unless governments in Europe – particularly in countries such as France and Italy – engage in more fundamental and often unpopular structural reforms, there is a danger that the European economy will continue to slide sideways (only this week, the European Commission downgraded its growth forecasts for the EU and eurozone from poor to terrible).

If that happens, capital markets union will become a second order problem and could be kicked into the long grass. After all, it’s not as if the people of Europe have been marching in the streets demanding capital markets union (‘What do we want? Capital markets union. When do we want it? Now…’).

It is also worth remembering that capital markets union is just one of three parts of Jonathan Hill’s job description: his full title is Commissioner for Financial Stability, Financial Services and Capital Markets Union. If and when a banking crisis erupts again in Europe, it’s fairly safe bet capital markets union brief would be put on hold.

2- If it ain’t broke…

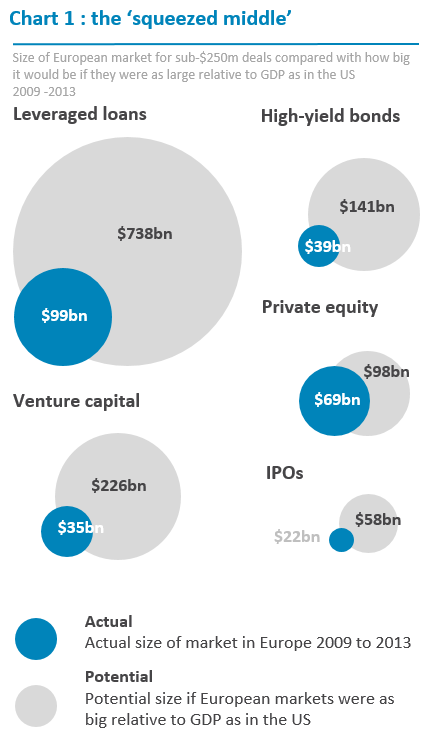

There is a danger of assuming that everything about capital markets in Europe needs fixing. Of course, capital markets are very underdeveloped in Europe relative to the US – our own research showed they are about half the size relative to GDP as they are in the US, and in some areas such as high-yield bonds, leveraged loans and securitisation, they are less than one third the size. For medium sized companies, capital markets in Europe are one fifth the size as in the US. (see our research on the depth of capital markets in Europe and the US here)

But many parts of the capital markets in Europe work well. For example, big investment grade issuers do not have a problem tapping the capital markets, and so far this year the value of equity issuance in Europe is around 15% higher than in the US and the value of European IPOs is nearly one third higher. Other markets, such as high yield bonds, are growing fast.

There is a natural tendency to focus on the obstacles to the free flow of capital in Europe, when sometimes it might be worth reflecting on the remarkable progress that has been made over the past 20 or 30 years towards creating a single capital markets in Europe. There are lots of examples of harmonisation – such as banking union, UCITS funds or standardised documentation in the loan and high-yield markets – that we take for granted but which highlight what can be achieved, and quickly, when there is a clear market need and when policymakers and the markets put their heads together.

3 – Laundry list

Capital markets union could rapidly descend into a long and unwieldy laundry list. Any attempt to push through wholesale cultural, institutional and legislative change over the next few years would probably be counterproductive. For example, we looked at five different reports on capital markets and long-term financing in Europe (by the European Commission, the Association for Financial Markets in Europe, the City of London, the Centre for European Reform, and New Financial) and counted a minimum of 99 policy recommendations. Let’s call it 100. Even if you strip out the duplication, there are at least 50 separate policy recommendations already out there (all of the recommendations are at the bottom of this article).

Instead it would be better to select a handful of tactical reforms that strike the right balance between a) being achievable and b) having a concrete, measurable and significant impact. How to select these priorities – when different parts of the industry and different countries have such fiercely held views – is the multi-billion euro question. A good starting point would be to identify and mobilise those organisations that demonstrably struggle to access or deploy capital effectively – such as medium-sized European corporates and pension funds.

4 – Too much regulation

There are plenty of people in Brussels for whom no problem is so complicated that it cannot be solved without more regulation or another directive. Add to that the reflexive urge of many politicians to regulate – and the legislative hyperactivity of Hill’s predecessor Michel Barnier – and you have a recipe for a potential barrage of new regulation and additional structures around capital markets union.

Instead, the focus of capital markets union should be on removing the existing barriers to the free flow of capital across borders in Europe, on finishing what the European Commission has already started, and on measuring the benefit, cost and impact of existing rules before writing new ones.

It is encouraging to see that Hill has so far shown he is inclined not to be rushed. In his speech at the conference today, he stressed that while there was not going to be a bonfire of financial regulations, he would pause to reflect on whether the European Commission has the right-balance between reducing risk and encouraging growth. Hill has said he will focus on a small number of areas and work out the individual and cumulative effects of existing legislation and regulation, before putting together an action plan by the end of summer 2015.

5 – Too ambitious

Capital markets union is not an opportunity to solve problems that have eluded policymakers since the Treaty of Rome in 1957 or the Single Market Act of 1986 (when the freedom of movement of capital was named as one of the four main ‘freedoms’ along with people, goods and services on the first page of the treaty). Trying to do much – for example, by trying to harmonise entire areas of tax and company law at the same time – would be a recipe for failure. Trying to do it too soon could also hole the project before it has even got started. Do we need an action plan by the middle of 2015? Does that leave enough time to really think through the challenges and priorities? We have waited more than 20 years since the official launch of the single market – so what’s the rush?

The danger here is that capital markets union pursues the desirable rather than the achievable. Harmonising withholding tax regimes or the unequal tax treatment of debt and equity across Europe would have a transformative effect, as would harmonising insolvency regimes and bankruptcy laws across Europe (click here for a terrifying look at the differences in existing law). But Hill and his team would probably have better luck achieving world peace and abolishing global poverty.

6 – Not ambitious enough

Alternatively, the Commission may not be ambitious enough. Hill might take one look at the sheer scale and complexity of the problem and decide that it would far safer just to carry on what has already been started in terms of a single capital market, and perhaps tinker at the edges with some achievable but unspectacular reforms.

Hill has already said that his priority is to finish what has been started, and that there are some obvious initiatives such as ELTIFs (European long-term investment funds) and pushing ahead with the development of a private placement market, on which work can start immediately. It might be best to see how those two initiatives work out before setting anyone’s expectations too high.

7 – Wrong diagnosis

If you misdiagnose the problem then it is unlikely that the treatment will work. A lot of focus has been on primary capital markets when the bigger problems may be in the secondary markets that you need to support them.(ref. the recent volatility in the US bond markets, or the high costs of cross-border clearing and settlement in Europe).

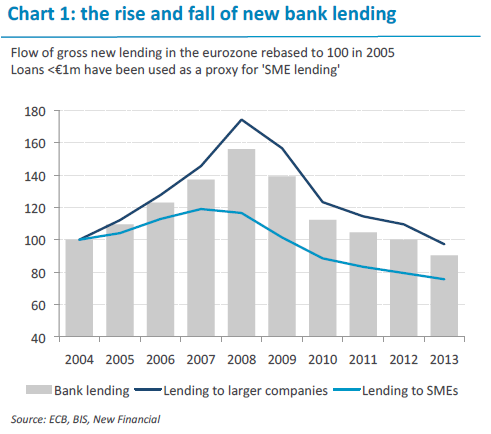

There is also a widely held assumption that the decline in bank lending is a problem in itself and that many companies – particularly SMEs – are being unjustly starved of credit. If you accept that banks lent too much money too loosely before the crisis – not a controversial view – then you have to accept that a large part of the 40%+ fall in new bank lending to SMEs in Europe is a healthy adjustment.

Equally, policymakers should beware of blindly copying the US model (in which 80% of corporate funding comes from capital markets compared with just 20% in Europe) when the institutional and cultural framework is so different. There is also a risk that the European Commission and European Parliament will focus too much on ‘union’ (ie harmonising rules and regulations) and not enough on ‘capital’ or ‘markets’.

8 – Diving in headfirst

Filling whatever funding gap may exist in Europe is not as easy as it looks. For all of the noise and political impetus behind ‘direct lending’ – in leveraged loans, private placements or infrastructure investing – some asset managers are finding that they don’t have the right skills and expertise and that it is harder than it looks. Innovations such as crowdfunding and P2P lending have made impressive progress, but perhaps it is best to reserve judgement on whether they will displace traditional banking models until after interest rates have gone up a few notches?

Dedicated SME or growth stockmarkets look and sound great – but they are a tiny source of funding. IPOs of less than $100m in Europe raised just $13bn in the five years to 2013. That’s less than $3bn a year, or a few days worth of new SME bank lending in Europe.

9 – Playing politics

Politics could also get in the way. There is a risk that some ideas which have captured the political imagination – such as the securitisation of SME loans or initiatives to build growth stockmarkets – could be rushed through the system with unrealistically high expectations in order to show that ‘something is being done’.

Reform could also become politicised, with pensions assets being allocated (or more accurately ‘appropriated’) for infrastructure investment, or particular countries insisting on particularly difficult policies as a quid pro quo for getting what they really want or (worse) as a subtle means of torpedoing the entire project. For example, the finance minister of country recently said capital markets union ‘must’ include the harmonisation of insolvency law – which is about as likely as getting Nigel Farage to vote in favour of a bigger EU budget next year.

If in doubt, look at the vote in the European Parliament against the appointment of Hill as a commissioner, for no other apparent reason than the fact that he was a) British and b) might have once advised a bank on its PR.

10 – A circular firing squad

The financial markets industry is perfectly capable of stealing defeat from the jaws of victory. It might try to use the need for growth as an excuse to sidestep painful reforms and to press pause on all of this touch-feely culture and trust stuff.

Even supporters of liberal capitalism and free markets have lost faith in many aspects of the industry (see the excellent the recent speech by Minouche Shafik at the Bank of England: ‘well-functioning markets are the key to prosperity but they must operate in ways that are fair and effective to sustain public support and confidence’).

All sectors of the industry will need to make concrete efforts to reform themselves and rebuild trust – with policymakers, with clients and with each other – to prove that they can be let out on a longer leash. As Hill said today, the industry must engage more constructively if it wants policymakers to champion its role and contribution. And the industry will need to overcome squabbling between different sectors over policy priorities that could stop capital markets union in its tracks.

PART 3 – APPENDIX – SUMMARY OF RECOMMENDATIONS OF DIFFERENT REPORTS

We have read five different reports on capital markets and long-term financing in Europe so that you don’t have to, and summarised their policy recommendations. All 99 of them.

European Commission: Long-term financing of the European economy

March 2014

- Support the development of pensions schemes in the EU

- Encourage the development of crowdfunding and P2P lending

- Structural reforms to banking remove distortions and boost lending to the real economy

- Review the impact of capital and liquidity requirements on long-term lending

- Review the impact of capital requirements in insurance sector on long-term investment

- Review and remove national restrictions on types of assets that insurance funds can invest in

- Review and remove national restrictions on types of assets that pension funds can invest in

- Move towards development of single market for personal pensions

- Encourage the cross-border retail savings market

- Increase the role and harmonisation of national development and promotional banks

- Improve the collaboration between different national export agencies and guarantees schemes

- Minimise regulation burden in capital markets for SMEs

- Help develop liquid and transparent corporate bond markets

- Open up UCITS structures to investing in SMEs and unlisted securities

- Open up ELTIFS (European Long-Term Investment Funds) to investing in SMEs

- Help develop a ‘high quality’ securitisation market

- Review the impact of capital requirements on the covered bond market and encourage development of a European covered bond market

- Review best practice and remove obstacles to help develop a European private placement market

- Create a pan-European SME credit database

- Improve transparency in infrastructure procurement process and around credit history of existing infrastructure projects

- Review shareholders rights directive to ensure better alignment with longer-term financing

- Review the impact of accounting standards on long-term financing

- Review the preferential tax treatment of equity vs debt

- Review potential ways of harmonising insolvency and bankruptcy law

Association for Financial Markets in Europe / Oliver Wyman: Unlocking funding for European investment and growth

June 2013

- Develop role of national promotional banks

- Improve allocation and distribution of existing EU funds

- Creation of a pan-European credit database / register for SMEs

- Explore development of high quality securitisation market for SME loans

- Development of credit mediation agencies

- CGT relief on SME investments

- Tax relief on equity financing for SMEs

- Clarify application and impact of Mifid on SME market financing

- Review impact of capital requirements on derivatives

- Review impact of clearing rules

- Develop and expand private placement market

- Standardise disclosure regimes for Hhigh-yield markets

- Improve harmonisation of European insolvency laws

- Harmonisation of withholding tax

- Increase transparency of planning and pipeline in infrastructure

- Expand existing Project Bond Initiative

- Develop EU-wide guidelines on political and regulatory risk of infrastructure projects and harmonise tendering process

- Increase government guarantees for early stage infrastructure projects

- Review impact of capital requirements on commercial real estate financing

- Create a pan-European REIT structure

- Improve education of non-bank investors about CRE

- Consider exemption from 5% retention rule for CLO managers with a high quality governance

- Review impact of capital requirements on key asset classes for pensions and insurers

- Review and address counter-cyclicality in pensions and insurance regulation

- Create legal framework for LTIFs (long-term investment funds)

- Encourage better information sharing and consistency on non-traditional asset classes

City of London: Financing Europe’s Investment and Economic Growth

(Llewellyn Consulting for IRSG, City of London, The CityUK, ParisEuroplace)

June 2014

- Encourage development of venture capital markets

- Encourage development of high yield and leveraged loan market

- Encourage development of SME / growth stockmarkets

- Encourage development of private placement market

- Identify and help plug the ‘growth funding gaps’ as companies move from start-up to SME to medium-sized company

- Encourage the development of corporate bond exchanges

- Review the impact of the fragmentation in insurance and pensions markets

- Review mark to market accounting and impact on short-termism

- Address concerns over regulatory uncertainty

- Encourage greater standardisation of documentation / process

- Encourage development of equity rather than debt financing

- Expand role of national development banks

- Encourage greater transparency in financial instruments

- Avoid heavy-handed regulation

- Be wary of structural separation in the banking industry

- Develop a better understanding by policymakers of how banks functions

- Encourage the growth of positive elements of shadow banking

- Define shadow banking more clearly and improve transparency

- Ensure regulation enhances complementary nature of shadow banking

- Increase the range of accepted collateral for clearing and central banks

- Shift emphasis of securitisation away from mortgage-backed securities towards SME bank loans

- Develop high quality securitisation market

Centre for European Reform: Unlocking Europe’s capital markets union

October 2014

- Encourage the development of high quality securitisation market

- Encourage the development of direct lending by pension funds, insurance companies and other ‘shadow banks’

- Support the growth of P2P lending and crowdfunding

- Introduce passport system for shadow banking (to overcome national restrictions on ‘lending’)

- Create a European credit risk database for SMEs

- Introduce greater transparency and clarity in planning and procurement process for infrastructure projects

- Review and remove national restrictions on pensions / insurance funds investing in certain asset classes

- Review regulation of credit rating agencies to encourage corporate bond market

- Develop standardised documentation for bond prospectuses

- Review and disincentivise cross-subsidisation of bank loans for bigger clients (which discourage their use of the capital markets for vanilla funding)

- Encourage the development of a European private placement market and minimise disclosure requirements for more sophisticated borrowers and investors

- Address the discriminatory tax treatment of equity versus debt

- Encourage the development of ELTIFs, with particular emphasis on supporting venture capital

- Review and reduce restrictions on UCITS funds investing in un-listed companies

- Expand use of tax-breaks to encourage high net worth investment in venture capital / SMEs

- Review US scheme of government guarantees for debt issued by smaller companies

- Abandon the FTT (financial transaction tax) and adopt a FAT (financial activity tax, based on profits, VAT, revenues and balance sheet)

New Financial: Driving growth – making the case for bigger and better capital markets

September 2014

- Define scope, ambition and metrics for ‘capital markets union’

- Develop more consistent data collection for SMEs and pension funds in Europe

- Focus less on expanding access to capital markets for SMEs and more on ‘squeezed middle’ companies between $50m to $250m.

- Focus on developing institutional loan market (ie. loans not held on bank balance sheets)

- Encourage creation of longer-term pools of capital, such as auto-enrolment / compulsory funded pensions schemes.

- Review and remove national restrictions on pensions / insurance and certain types of fund investing in certain assets

- Work on co-ordinating and linking a lot of the work already done at a national level in creating listed bond markets and SME / growth stockmarkets

- Focus on developing minimum thresholds for regulation, instead of maximum levels of harmonisation

- Review impact and effect of existing regulation and if necessary repeal or rewrite it

- Focus on the ‘decomplexification’ of capital markets and encourage greater clarity, consistency and transparency across the industry